Ilya Spivak, On Friday 25 November 2011, 10:33

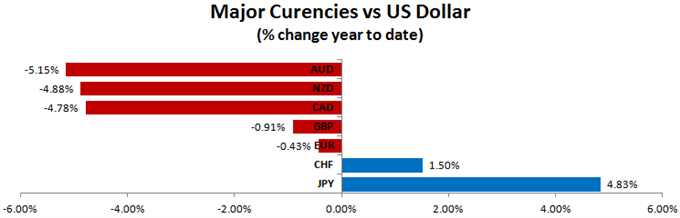

The Australian, Canadian and New Zealand Dollars – the so-called “commodity bloc” – have been the worst performers against their US namesake among the majors so far this year.

The Australian, Canadian and New Zealand Dollars – the so-called “commodity bloc” – have been the worst performers against their US namesake among the majors so far this year. The outcome reflects the group’s sensitivity to global economic growth expectations and investors’ risk appetite at a time when the post-2008 crisis faces its most considerable headwinds yet, with output expansion increasingly expected to slow worldwide while the Euro Zone sovereign debt crisis threatens to unleash another credit disaster onto financial markets.

Source: Bloomberg

Drivers of the Commodity Currencies

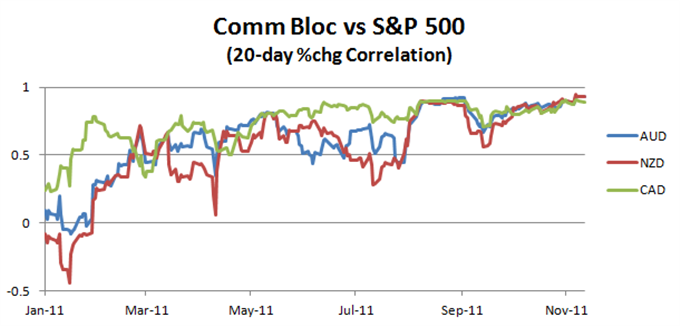

The fundamental forces behind the Australian, Canadian and New Zealand Dollars are clearly revealed in the currencies’ intimate correlation with the S&P 500 benchmark stock index over recent years. An understanding this relationship illustrates precisely why the commodity currencies were so strong on the way out of the Great Recession previously and whey they’ve lost their appeal so dramatically this year.

What does the S&P 500 represent?

Put simply, it is a reflection of the markets’ collective expectations of future earnings for the world’s largest companies. Looking past the minutiae of individual firms and evaluating the aggregate, those expectations are naturally a function of what investors believe about the pace of global economic growth. Naturally enough, if growth is expected to be robust, earnings are likely to rise as companies find more opportunities to do business as well as greater demand for their goods and services. Needless to say, the reverse is likewise the case.

Taking this logic one step further, it seems reasonable enough to say that growth expectations will probably be quite telling of the markets’ general appetite for risk. If aggregate earnings are expected to rise overall, investors will be comparatively more sanguine about taking additional risks for a chance at greater returns than they would if the global economy was in dire straits and uncertainties loomed large. Once again, the same logic applies in the opposite scenario as well. To this end, the S&P 500 is both a real-time proxy for the financial markets’ collective economic growth outlook as well as a barometer for their risk tolerance.

Source: Bloomberg

Why are commodity currencies aligned with the S&P 500?

All three economies look to exports of raw materials to the world’s top-two economic engines as their core source of expansion. In the case of Australia and New Zealand, that is China. The East Asian giant has a healthy appetite for Australian mining goods, most notably coal and iron ore, as well as New Zealand foodstuffs like meat and dairy. Meanwhile, Canada has a similar relationship with the United States. Indeed, close to 80 percent of Canadian exports are headed for US markets. Crude oil is an oft-cited focal point in this relationship, but other goods such as lumber are also important.

Needless to say, any given country’s economic growth outlook is an important determinant of its currency’s exchange rate. In the simplest of terms, strong performance puts upward pressure on the price of goods across the spectrum as growing demand chases after finite supply, driving inflation. Central banks seeking to cap price growth raise interest rates to encourage saving and discourage consumption in a bid to cool growth. Rising interest rates represent an increase in the return to be had for holding deposits in a given currency, driving investment demand and leading to appreciation.

If economic performance in Australia, Canada and New Zealand is determined by demand from the US and China, the long-term trajectory of their currencies are a function of that very same thing. Because the US and China happen to be the world’s first- and second-largest economies, the same can be said of the world as a whole, bringing us back to the S&P 500. All told, we can see that at their core, the Aussie, Kiwi and Canadian Dollars are no less a function of the very same global growth expectations and related risk appetite trends that drive the benchmark stock index.

Headwinds Facing Global Economic Growth, Risk Appetite

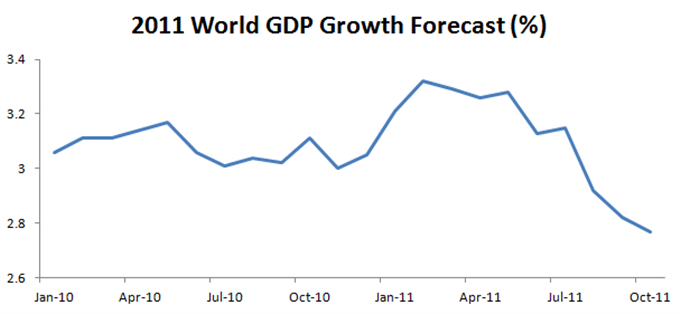

Having established what drives the commodity currencies, we turn to what undermined them as well as risk appetite at large in 2011. Broadly speaking, this brings us to two discrete themes: the slowdown in global economic growth and the lingering Euro Zone sovereign debt crisis.

The Global Recovery is Faltering

Turning first to global economic growth, it is clear that the markets have been faced with a deteriorating outlook for worldwide performance as all three of the world’s leading growth engines – the US, China and the Euro Zone – turn increasingly sluggish. The downturn in China is self-induced, while those in the West reflect the fading effects of aggressive fiscal and monetary stimulus efforts.

Source: Bloomberg

The administration in Beijing has struggled to contain inflation, with the annual growth rate of the Consumer Price Index hitting a three-year high by mid-year and hovering uncomfortably above the 6 percent threshold throughout the third quarter. Inflation poses a major problem for China’s rulers, who know all too well that the price of failing to secure affordable access to basic necessities for the country’s enormous population is often mass upheaval and regime change. As such, authorities moved to slow the economy and curb price growth with a total of 11 interest rate hikes so far this year, at times acting on the 1-year lending and/or deposit rates as well as banks’ reserve requirements. The results have been dramatic: the annual GDP growth rate slowed to the weakest in two years by the third quarter while the Manufacturing PMI gauge of factory-sector growth that approximates trends in the overall economy dropped to the weakest since February 2009 in October.

In the US, much of the damage occurred in the first half of the year, with GDP adding a paltry 0.4 percent in the first quarter followed by a still sub-par 1.3 percent in the three months through June. Meanwhile, a Citigroup metric tracking US economic data surprises sank to the lowest since late 2008 by mid-June. Much of this weakness can be traced to the disappearance of the boost from the government’s aggressive stimulus spending, but ripple effects from such events as the Tohoku earthquake in Japan that – for example – disrupted parts shipments to US auto manufacturers are likewise to blame. Performance seems to be improving in the second half of the year, but consensus annual GDP growth expectations compounded in a survey from Bloomberg suggest the economy will add 1.8 percent from the previous year in 2011, a marked slowdown from the 3 percent recorded in 2010.

Finally turning to Europe, the fading impact of stimulus measures and a lurch toward austerity on the fiscal side of the equation were compounded by added pressure from the European Central Bank in the monetary policy space. Mirroring its often-criticized decision to raise interest rates in the middle of 2008 as the global credit crunch was on the cusp of being unleashed onto financial markets, the ECB opted to react to rising headline with a cumulative 50bps in tightening between April and July. The results have been dramatic: economists’ 2011 economic growth expectations (as tracked by Bloomberg) topped out in June and began to trend firmly lower in August, now calling for the currency bloc’s GDP to add just 1.6 percent this year. The outlook for 2012 is even more ominous, with a paltry 0.7 percent increase set to underperform the rest of the G10 by a wide margin.

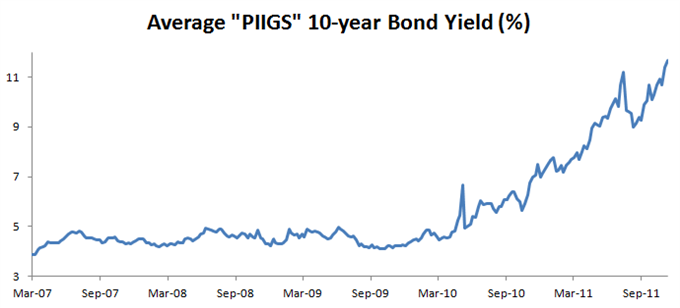

Euro Zone Debt Crisis Rekindles Meltdown Fears

Amplifying already substantial headwinds facing risk appetite is the return to the spotlight of Euro Zone sovereign debt crisis. The inability of some countries in the currency bloc to keep up with their debt obligations seemingly vanished from the foreground in 2010 after Greece and Ireland received €110 billion and €85 billion bailouts in May and November, respectively. This year seemed to start on a positive note when Eurozone finance ministers set up a permanent €500 billion bailout facility called the European Stability Mechanism (ESM), but stress returned as Portugal admitted it was underwater and asked for a rescue in April. It received a €78 billion lifeline in May, but another lull in market jitters was not to be.

In June, Eurozone finance threatened to withhold an aid payment to Greece unless the country agrees to commit to harsher austerity measures, sparking fears that a default within the currency bloc was imminent. Though the Greek Parliament approved further budget cuts and received the aid while Eurozone officials cobbled together a second €109 billion aid package by July aimed to fund Athens as well as prevent contagion elsewhere in the region, the situation began to spiral out of control. By August, yields on Spanish and Italian bonds began to soar as investors demanded a hefty premium to lend to the next set of Euro member states thought to come under sovereign pressure. The ECB reluctantly agreed to begin buying the two countries’ bonds in a bid to cap borrowing costs, but the effort proved too anemic to have a game-changing impact. A so-called “comprehensive” solution hashed out at a summit in October – proposing to write down 50 percent of privately-held Greek debt, lever up the existing €440 billion bailout fund (the European Financial Stability Facility, or EFSF) to €1 trillion, and require Eurozone banks to adhere to a 9 percent reserve requirement – failed to reassure investors. Likewise in November, short-lived sigh of relief following a change of governments in Greece and Italy is already running out of stream.

The debt crisis presents a two-pronged problem. On one hand, it amplifies already considerable headwinds facing Euro Zone economic growth. Soaring borrowing costs amid fears of a default within the currency bloc stymie growth as individuals and businesses find it more expensive to spend and invest. In turn, slower growth reduces regional governments’ tax intake, making it that much harder to reduce deficits, stoking already considerable sovereign solvency fears and producing a vicious cycle. On the other, it threatens to unleash another market-wide selloff and global credit crunch, plunging worldwide finance at large into another existential crisis just three years after the 2008 debacle.

Source: Bloomberg

Needless to say, the key threat is that of a default in a large country like Italy or Spain – the third- and fourth-largest economies in the Eurozone, respectively – where the problem is simply too big to be addressed with a Greece-style bailout. Indeed, Italy is the world’s third-largest bond market, meaning the impact of its default would prove far more detrimental than the now infamous collapse of US investment bank Lehman Brothers that triggered what would become the Great Recession. Countless banks, funds and other institutions would suddenly find their holdings of Italian bonds to be absolutely worthless and be forced to book sharp losses.--- Written by Ilya Spivak, Currency Strategist for Dailyfx.com

Eurozone stocks surge for second day on news of coordinated efforts by Federal Reserve and others central banks to ease the threat against the currrency Euro. Commodity currency Aud continue to soars to 3.27 against Myr.

Eurozone stocks surge for second day on news of coordinated efforts by Federal Reserve and others central banks to ease the threat against the currrency Euro. Commodity currency Aud continue to soars to 3.27 against Myr. Aud/Myr posted weekly gain of more than 5 % while

Aud/Myr posted weekly gain of more than 5 % while Although gold in USD actually soars 4 % to 1747 as US dollar weakens ...,

Although gold in USD actually soars 4 % to 1747 as US dollar weakens ...,

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)