May you guys and gals find great happiness in the year ahead.

Enjoy everlasting laughs and ever-laughing life... Be happy ......!

http://comedy.video.yahoo.com/?v=7652402

Friday, December 31, 2010

Wednesday, December 29, 2010

IJM Land. How to catch a falling knife

Catching a falling knife is not an easy task but here's what I did on IJM Land warrant

Yesterday closing price = RM1.89 Today opening at RM1.80 at 5% loss

First, place a huge position at 35% "limit-down" from opening price, ie. minimum price allowed is RM1.33

Subsequently, place positions at downwards increment of

6lot x 30% at RM1.38, 5lot x 25% at RM1.44, 4lot x 20% at RM1.50,

3lot x 15% at RM1.56, 2lot x 10% at RM1.63, 1lot x 5% at RM1.71

If my order is matched all the way down 30%, my average purchase is RM1.48 (21%), pretty much a good support range

If my order is matched down to 20%, my avg price would be 10 lot x RM1.565

Yesterday closing price = RM1.89 Today opening at RM1.80 at 5% loss

First, place a huge position at 35% "limit-down" from opening price, ie. minimum price allowed is RM1.33

Subsequently, place positions at downwards increment of

6lot x 30% at RM1.38, 5lot x 25% at RM1.44, 4lot x 20% at RM1.50,

3lot x 15% at RM1.56, 2lot x 10% at RM1.63, 1lot x 5% at RM1.71

If my order is matched all the way down 30%, my average purchase is RM1.48 (21%), pretty much a good support range

If my order is matched down to 20%, my avg price would be 10 lot x RM1.565

Sunday, December 26, 2010

TDM. Plantation governs

I think TDM will follow the path of HS Plant and IJM PLant... In the region of RM3.30 to RM3.40 If it is expected to pay Dv of 15 sen, then dividend yield = 15sen/RM3.00 = 5 %

I'm positive on plantations...... Just buy your favourites and watch it go up, up and away

I'm positive on plantations...... Just buy your favourites and watch it go up, up and away

Friday, December 24, 2010

Blessed Christmas & Happy New Year

Christmas is time when God's love descended on earth.

His name shall be called Prince of peace ( peace with God and man ), Wonderful Counsellor ( comforts man's soul/ grief ), Immanuel ( God dwelling with/in man).

For God so loved the world that He gave his only begotten Son so that whoever believes in Him shall have " ever-laughing life and everlasting laugh ."

May you always be happy... Im-Manu-El

Wednesday, December 22, 2010

IOI Corp is relatively cheap

IOI Corp ( nta 165, Q/Q 7.7/ 8.6/ 8.6/ 7.8 sen ) Fv = RM3.27

Paid 17 sen total dividend over last four quarters. Trading at RM 5.80 w/ PE 17.7

Relatively cheap and attractive when compared to same league plantation giant KLK trading at PE 21

It's a matter of time before IOI Corp share price goes ballistic....!

Paid 17 sen total dividend over last four quarters. Trading at RM 5.80 w/ PE 17.7

Relatively cheap and attractive when compared to same league plantation giant KLK trading at PE 21

It's a matter of time before IOI Corp share price goes ballistic....!

Monday, December 20, 2010

J Tiasa. THPlant

Seems like plantation sector is still very much in play/trade.

I'm looking at J Tiasa ( nta 431, Q/Q 1.2/ 5.1/ 3.4/ 8.4/ 11.3 sen)

Trailing annual EPS 28 sen. Trading at RM4.65 w/ PE 17, well, not my cup of tea...

THP ( 096, Q/Q 4.6/ 3.7/ 1.6/ 4.4 sen ) Fv = RM1.40

Trading at RM1.90 w/ PE 13.6 and w/ a dividend of 8.5 sen in 5 months time. Now this is something to seriously consider buying on price weakness...

Compare earnings w/ others:

Cepat ( 169, 1.6/ 2.7/ 2.5/ 1.3/ 4.1 sen ) Fv = RM1.06 Trading at RM1.40 w/ PE 13.2

RSawit ( 061, latest Qeps 3.8 sen) Trading at RM1.93

KMLoong ( 141, 4.8/ 3.9/ 4.4/ 3.9 sen) Fv = RM 1.70 Trading at RM2.56 w/ PE 15

IJMP ( 154, Q/Q 3/ 5/ 2/ 4/ 6 sen ) Fv = RM1.70 Trading at RM 2.95 w/ PE 17

HSP ( 213, Q/Q 3/5/4.5/ 4.5/ 5.2 sen) Fv = RM 1.90 Trading at RM 3.20 w/PE17

TSH ( 178, Q/Q 5.7/ 5/ 3/ 3/ 4.4 sen ) Fv = RM 1.60 Trading at RM 2.80 w/ PE 17.5

I'm looking at J Tiasa ( nta 431, Q/Q 1.2/ 5.1/ 3.4/ 8.4/ 11.3 sen)

Trailing annual EPS 28 sen. Trading at RM4.65 w/ PE 17, well, not my cup of tea...

THP ( 096, Q/Q 4.6/ 3.7/ 1.6/ 4.4 sen ) Fv = RM1.40

Trading at RM1.90 w/ PE 13.6 and w/ a dividend of 8.5 sen in 5 months time. Now this is something to seriously consider buying on price weakness...

Compare earnings w/ others:

Cepat ( 169, 1.6/ 2.7/ 2.5/ 1.3/ 4.1 sen ) Fv = RM1.06 Trading at RM1.40 w/ PE 13.2

RSawit ( 061, latest Qeps 3.8 sen) Trading at RM1.93

KMLoong ( 141, 4.8/ 3.9/ 4.4/ 3.9 sen) Fv = RM 1.70 Trading at RM2.56 w/ PE 15

IJMP ( 154, Q/Q 3/ 5/ 2/ 4/ 6 sen ) Fv = RM1.70 Trading at RM 2.95 w/ PE 17

HSP ( 213, Q/Q 3/5/4.5/ 4.5/ 5.2 sen) Fv = RM 1.90 Trading at RM 3.20 w/PE17

TSH ( 178, Q/Q 5.7/ 5/ 3/ 3/ 4.4 sen ) Fv = RM 1.60 Trading at RM 2.80 w/ PE 17.5

Wednesday, December 15, 2010

Cepat Wawasan Production Discrepancy

Plantation Cepat Wawasan recently posted its Nov month production.

Fresh fruit bunch ( ffb ) = 11,127 metric tons

Crude palm oil ( cpo ) = 6,613 metric tons

Industry standard extraction rate is 21% so CPO should be 0.21 x 11,127 = 2,337 mt

I'm wary of the monthly CPO figure. Can anybody throw some light into this...?

Fresh fruit bunch ( ffb ) = 11,127 metric tons

Crude palm oil ( cpo ) = 6,613 metric tons

Industry standard extraction rate is 21% so CPO should be 0.21 x 11,127 = 2,337 mt

I'm wary of the monthly CPO figure. Can anybody throw some light into this...?

Tuesday, December 14, 2010

Commodities governs: Plantations Up Up

It's great to be back after a short holiday. I'm glad to see that many plantation's share price has moved, up up up. Justified coz palm oil may in the future be big big big revenue earner for the Gov't. Justified when you look at how much the commodity currency AUD, Gold, CPO future has spiked...! Go walk your local supermarket and check out the food prices...

My holding of QL Reso has gain me much though I wish I had bought into more eggs producing, farming, dairy products and poultry companies...

Anyway, I'm delighted for my positions in TDM, Kfima... still accumulating...

At this moment, I'm fond of TH Plant, HS Plant, IJMP with its warrant. Watch HS Plant and TSH and you can get a fairly good idea where IJMP and THP might be heading.. Though TSH is overpriced in my opinion...

Tips: Look for plantations whose share prices hasn't escalated by 20 %... Then buy...

Happy stock picking..!

My holding of QL Reso has gain me much though I wish I had bought into more eggs producing, farming, dairy products and poultry companies...

Anyway, I'm delighted for my positions in TDM, Kfima... still accumulating...

At this moment, I'm fond of TH Plant, HS Plant, IJMP with its warrant. Watch HS Plant and TSH and you can get a fairly good idea where IJMP and THP might be heading.. Though TSH is overpriced in my opinion...

Tips: Look for plantations whose share prices hasn't escalated by 20 %... Then buy...

Happy stock picking..!

Thursday, December 2, 2010

News Brief. IJM. TM. Glomac

IJM-JAKS JV wins RM269m water pipes contract for Pahang-Selangor raw water transfer project. No wonder IJM share price surge more than 5%, closing at RM6.13. I sold off some holdings. Could move up much higher on so much of the positive news of IJM Land. ...

Palm oil futures surge to 28 months high of RM3,523. OSK ups the average selling price in 2011 from RM2250 to RM2700

TM will sell entire 2.27 % stake in Axiata via a private placement, expecting to rake in 191.458 million shares x RM4.593 = RM 879.4m

Glomac ( nta 196, Q/Q 3.3/ 3.6/ 4.2/ 5.3/ 5.4 sen ) Fv 180

Palm oil futures surge to 28 months high of RM3,523. OSK ups the average selling price in 2011 from RM2250 to RM2700

TM will sell entire 2.27 % stake in Axiata via a private placement, expecting to rake in 191.458 million shares x RM4.593 = RM 879.4m

Glomac ( nta 196, Q/Q 3.3/ 3.6/ 4.2/ 5.3/ 5.4 sen ) Fv 180

Wednesday, December 1, 2010

HDD manufacturers may have tough time

Notion Vtec did a consolidation exercise many many months back. If memory serves me well, it was 5 shares into 1, which saw the new share price rising to new high. Technical charts points to higher share prices of Notion Vtec..

Many made their money rightfully during the euphoria and the excitement was turn to Dufu and listing of JCY. Not long after that, an article came forth that devastated the hope of HDD and HDD components maker.

I think it's the article that derails the fortune of the HDD industry though I may be wrong. Since then, I never touched the HDD co. shares and have observed its Q eps sliding. So it does pay to read a little and be observant.

What was the key item in the news article that rattle the counters of HDD makers in general...?

For fun, 100 credit points to the first 10 persons who got it right within 1 week from 2 Dec to 9 Dec.. 100 credit points earn you 1 month of my simple financial views and trading ideas sent personally to yr email bf it hit my blog. This posting will be deleted on 9th Dec...

(Remember to leave yr email and mobile no.. Thanks guys)

Clue: A fruit. Solid + no moving parts.

Many made their money rightfully during the euphoria and the excitement was turn to Dufu and listing of JCY. Not long after that, an article came forth that devastated the hope of HDD and HDD components maker.

I think it's the article that derails the fortune of the HDD industry though I may be wrong. Since then, I never touched the HDD co. shares and have observed its Q eps sliding. So it does pay to read a little and be observant.

What was the key item in the news article that rattle the counters of HDD makers in general...?

For fun, 100 credit points to the first 10 persons who got it right within 1 week from 2 Dec to 9 Dec.. 100 credit points earn you 1 month of my simple financial views and trading ideas sent personally to yr email bf it hit my blog. This posting will be deleted on 9th Dec...

(Remember to leave yr email and mobile no.. Thanks guys)

Clue: A fruit. Solid + no moving parts.

Tuesday, November 30, 2010

Plantations. CPO up

HS Plantation soared highest RM3.32 this Wednesday morning with an 18% gain in my portfolio. Sold some holdings.

TDM Plant din budge at all despite the fantastic quarterly EPS. Disappointment to many (including me) who bought in anticipating good Qeps and surge in price. I think TDM will follow the path of HSP, pauses at RM2.40 level bf breaking out higher. Syndicates, pls come and make my day..!

Kfima also reverses after I bought in. Anyway, no fretting. Keep looking for undervalued companies to buy into. Checking into IJMP and TSH.

Sorry, I dont like big plantation co. trading at high PER. KLK ( nta 564, Q/Q 23/ 23/ 20/ 23/ 29 ) Fv = 950. Now trading at RM20.20 w/ PE of 21, too high for my liking...

Meanwhile CPO prices has recovered from recent low, even surpassing recent high of RM3370 to RM3,415

My CMMT took a turn and surged to RM1.14 ( +5.5% ) at yesterday closing.

IJM spiked past RM6.00 ( +4.5% ) but slumped back RM5.74. Still more upside to come.

TDM Plant din budge at all despite the fantastic quarterly EPS. Disappointment to many (including me) who bought in anticipating good Qeps and surge in price. I think TDM will follow the path of HSP, pauses at RM2.40 level bf breaking out higher. Syndicates, pls come and make my day..!

Kfima also reverses after I bought in. Anyway, no fretting. Keep looking for undervalued companies to buy into. Checking into IJMP and TSH.

Sorry, I dont like big plantation co. trading at high PER. KLK ( nta 564, Q/Q 23/ 23/ 20/ 23/ 29 ) Fv = 950. Now trading at RM20.20 w/ PE of 21, too high for my liking...

Meanwhile CPO prices has recovered from recent low, even surpassing recent high of RM3370 to RM3,415

My CMMT took a turn and surged to RM1.14 ( +5.5% ) at yesterday closing.

IJM spiked past RM6.00 ( +4.5% ) but slumped back RM5.74. Still more upside to come.

Friday, November 26, 2010

TM. TDM. B'Stead. GenM. Earnings

B'Stead ( nta 435, Q/Q 12/ 16/ 10/ 16/ 10 sen ) Fv = RM4.00 Now trading at RM5.20 w/PE 13. Dividend 12 sen ex 14th Dec.

GenM ( nta 196, Q/Q 6/ 6/ 5/ 5/ 6 sen ) Fv = RM2.40 Now trading at RM3.20 w/PE 13

TM ( nta 209, Q/Q 5/ 5/ 7/ 3.5/ 12 sen ) Fv = RM 2.00. Trading at RM3.30 w/PE 17

TDM ( nta 303, Q/Q 9/ 10/ 9/ 6/ 13 sen ) Fv = RM4.80 Now trading at RM2.40 w/PE 5

GenM ( nta 196, Q/Q 6/ 6/ 5/ 5/ 6 sen ) Fv = RM2.40 Now trading at RM3.20 w/PE 13

TM ( nta 209, Q/Q 5/ 5/ 7/ 3.5/ 12 sen ) Fv = RM 2.00. Trading at RM3.30 w/PE 17

TDM ( nta 303, Q/Q 9/ 10/ 9/ 6/ 13 sen ) Fv = RM4.80 Now trading at RM2.40 w/PE 5

Sunway & Suncity: Which to buy...?

A fren today asked which to buy and at what price..? Here's a guide..

Generally, it's a buy when market price is below Sunway Sdn Bhd's offer price. Yet you want to buy at a huge discount cos' you're going to be holding the risk of market downturn from now until Sunway SB merge the two listed companies Sunway Holdings Bhd & Sunway City Bhd into a new company and relist it in Bursa ( possibly next year.?).

Trading in Sunway and it's warrant may be more liquid but you want to observe which gives the best discount if you intend to buy and hold till relisting of new company.

1). We all know the offer price for Sunway is RM2.60 and Sunway warrant WC is RM1.50

Mkt price today for Sunway is RM2.27 lowest and Sunway WC is RM1.28 lowest so Sunway is traded today's low at (260/227 => 1.145 ie, 14 % below offer price) and warrant is traded at (150/128 =>1.172 ie 17 % discount)

2). Offer price for Suncity is RM5.10 and Suncity warrant WA is RM1.29

Mkt price traded today for Suncity is RM4.49 lowest (510/449 => 1.136 ie 13 %) and for warrant WA is RM1.11 lowest (129/111 => 1.162 ie 16 % )

Here's a guide for a 20% off from offer price (2.60/ 1.50/ 5.10/ 1.29) for easy trading:

Sunway at RM2.16 Sunway-WC at RM1.25

Suncity at RM 4.25 Suncity-WA at RM1.07

Generally, it's a buy when market price is below Sunway Sdn Bhd's offer price. Yet you want to buy at a huge discount cos' you're going to be holding the risk of market downturn from now until Sunway SB merge the two listed companies Sunway Holdings Bhd & Sunway City Bhd into a new company and relist it in Bursa ( possibly next year.?).

Trading in Sunway and it's warrant may be more liquid but you want to observe which gives the best discount if you intend to buy and hold till relisting of new company.

1). We all know the offer price for Sunway is RM2.60 and Sunway warrant WC is RM1.50

Mkt price today for Sunway is RM2.27 lowest and Sunway WC is RM1.28 lowest so Sunway is traded today's low at (260/227 => 1.145 ie, 14 % below offer price) and warrant is traded at (150/128 =>1.172 ie 17 % discount)

2). Offer price for Suncity is RM5.10 and Suncity warrant WA is RM1.29

Mkt price traded today for Suncity is RM4.49 lowest (510/449 => 1.136 ie 13 %) and for warrant WA is RM1.11 lowest (129/111 => 1.162 ie 16 % )

Here's a guide for a 20% off from offer price (2.60/ 1.50/ 5.10/ 1.29) for easy trading:

Sunway at RM2.16 Sunway-WC at RM1.25

Suncity at RM 4.25 Suncity-WA at RM1.07

Thursday, November 25, 2010

Earnings, Earnings, Earnings

KFima ( nta 163, Q/Q 3.8/ 6.9/ 4.7/ 6.6/ 5.6 sen) Fv = RM2.20

TH Plant ( nta 096, Q/Q 2.6/ 4.6/ 3.7/ 1.6/ 4.4 sen ) Fv = RM1.40

HS Plant ( nta 213, Q/Q 3/ 5/ 4.5/ 4.5/ 5.2 sen ) Fv = RM2.00

IJM P ( nta 154, Q/Q 3/ 5/ 2/ 4/ 6 sen) Fv = RM2.40

HS Cons ( nta 441, Q/Q 7/ 2/ 7/ 24/ 8 sen ) Fv = RM 3.20

IJM ( nta 378, 7/ 6/ 8/ 7/ 9 sen) Fv = RM3.60

IJM L ( nta 150, Q/Q 3/ 2/ 2/ 5/ 3 sen ) Fv = RM 1.20

IGB ( nta 196, Q/Q 3/ 2/ 2/ 3/ 3 sen) Fv = RM1.20

RCECap ( nta 051, Q/Q 2.5/ 2.7/ 2.9/ 3/ 4 sen) Fv = 1.30

Axiata ( nta 228, Q/Q 6/ 7/ 11/ 7/ 8 sen ) Fv = RM 3.20

Lion Ind ( nta 420, Q/Q 10/ 12/ 12/ 17/ -3) loss making

QL Reso ( nta 140, Q/Q 8/ 9/ 7/ 7/ 8 sen) Fv = 3.20

DRB Hcm ( nta 250, Q/Q 3/ 5/ 13/ 8/ 7 sen ) Fv = 2.80

GenM (nta 196, Q/Q 6.3/ 6.3/ 4.8/ 5.3/ 5.9 sen Nov ) Fv = RM2.40

TH Plant ( nta 096, Q/Q 2.6/ 4.6/ 3.7/ 1.6/ 4.4 sen ) Fv = RM1.40

HS Plant ( nta 213, Q/Q 3/ 5/ 4.5/ 4.5/ 5.2 sen ) Fv = RM2.00

IJM P ( nta 154, Q/Q 3/ 5/ 2/ 4/ 6 sen) Fv = RM2.40

HS Cons ( nta 441, Q/Q 7/ 2/ 7/ 24/ 8 sen ) Fv = RM 3.20

IJM ( nta 378, 7/ 6/ 8/ 7/ 9 sen) Fv = RM3.60

IJM L ( nta 150, Q/Q 3/ 2/ 2/ 5/ 3 sen ) Fv = RM 1.20

IGB ( nta 196, Q/Q 3/ 2/ 2/ 3/ 3 sen) Fv = RM1.20

RCECap ( nta 051, Q/Q 2.5/ 2.7/ 2.9/ 3/ 4 sen) Fv = 1.30

Axiata ( nta 228, Q/Q 6/ 7/ 11/ 7/ 8 sen ) Fv = RM 3.20

Lion Ind ( nta 420, Q/Q 10/ 12/ 12/ 17/ -3) loss making

QL Reso ( nta 140, Q/Q 8/ 9/ 7/ 7/ 8 sen) Fv = 3.20

DRB Hcm ( nta 250, Q/Q 3/ 5/ 13/ 8/ 7 sen ) Fv = 2.80

GenM (nta 196, Q/Q 6.3/ 6.3/ 4.8/ 5.3/ 5.9 sen Nov ) Fv = RM2.40

Wednesday, November 24, 2010

Sunway Holdings to merge with Sunway City

Sunway Sdn Bhd will acquire the two listed construction and property outfits, Sunway Holdings Bhd at RM 2.60/ share and Suncity Bhd at RM 5.10/ share, merge and relist it in Bursa with NEW CO shares at RM2.80/share with cash repayment and free warrants.

My gain/profit of Suncity shares is now up by 27 %

My greatest gain on my purchase since my previous posting on 18th October: Sunrise (30%), Suncity (27%), Masteel (24%). My disappointment has got to Leader Universal: it reverses after my purchase.

Someone tease if I could manage their portfolio. I jokingly asked if he would be willing to pay 2% charge on stocks purchase and 20% charge on all profit/gain made. that's what most fund manager charges 2: 20 rule.

Nay, it's far cheaper to just read and follow my blog and many other excellent blogs. Beside there are many TA guys/frens who made much much more trading the market. A close fren consistently makes RM4,000 on his capital of RM40,000 over 2 months. That's 5% monthly average or 60% a year. I could never ever beat that record coz I'm more like a "turtle investor" rather than a speculative trader.

Happy stock picking...!

My gain/profit of Suncity shares is now up by 27 %

My greatest gain on my purchase since my previous posting on 18th October: Sunrise (30%), Suncity (27%), Masteel (24%). My disappointment has got to Leader Universal: it reverses after my purchase.

Someone tease if I could manage their portfolio. I jokingly asked if he would be willing to pay 2% charge on stocks purchase and 20% charge on all profit/gain made. that's what most fund manager charges 2: 20 rule.

Nay, it's far cheaper to just read and follow my blog and many other excellent blogs. Beside there are many TA guys/frens who made much much more trading the market. A close fren consistently makes RM4,000 on his capital of RM40,000 over 2 months. That's 5% monthly average or 60% a year. I could never ever beat that record coz I'm more like a "turtle investor" rather than a speculative trader.

Happy stock picking...!

Tuesday, November 23, 2010

Resources Fund Price Reverses

Osk Uob Resources unit fund price dived from recent peak of 70 sen to 67.14 sen within 10 days, taking a 5 % loss. Among its investment poftfolio are agribiz giant Wilmar SG ( share price nosediving 12 %) and both mining giants BHP (AU) and RIO (AU) taking 5 % drop in share prices. CPO price also continue to dip from recent high of RM3370 to RM3115 ( 8 % )

Monday, November 22, 2010

China Raises Banking Reserves, Contains Inflation.

DJ Newswires: Effective 29th Nov, China Central Bank will raise banks reserve ratio requirement, intensifying efforts to drain excess liquidity from the banking system to rein in credit growth after China's consumer price inflation shot up to 4.4%

Bad news for commodities.

Commodities currency AUD slid from 3.13 to approx 3.06

CRB Index retreats from 314 to 299. CPO price drops from 3370 to 3180.

Thursday, November 11, 2010

My Profitable Investment Over Last 3 Months

Plantations:

Bought Boustead at RM 4.30 and still accumulating ( gain 32% at RM 5.70 today )

TDM at RM 2.15 & 2.41 and still accumulating ( up 10% at RM 2.50 )

HS Plant at RM 2.79 and still accumulating ( up 8 % at RM 3.02 )

I'll evaluate another few counters in this sector and then take some position in them.

Properties & Building Materials:

Sunrise at RM 2.13 ( up 48 % at RM 3.16 )

Suncity at RM4.00 and accumulating ( up 2 % at RM 4.08)

MaSteel RM0.85 ( up 21 % at RM 1.02 )

Leader RM 0.88 and accumulating ( up 2 % at RM 0.90 )

Likes Ann Joo. Loves South Steel even more but unfortunately capped in price.

I have posted the fundamentals on the above stocks so the price movement should trend upwards in the medium term.

My loser: TM and CMMT ( down 2 % )

Bought Boustead at RM 4.30 and still accumulating ( gain 32% at RM 5.70 today )

TDM at RM 2.15 & 2.41 and still accumulating ( up 10% at RM 2.50 )

HS Plant at RM 2.79 and still accumulating ( up 8 % at RM 3.02 )

I'll evaluate another few counters in this sector and then take some position in them.

Properties & Building Materials:

Sunrise at RM 2.13 ( up 48 % at RM 3.16 )

Suncity at RM4.00 and accumulating ( up 2 % at RM 4.08)

MaSteel RM0.85 ( up 21 % at RM 1.02 )

Leader RM 0.88 and accumulating ( up 2 % at RM 0.90 )

Likes Ann Joo. Loves South Steel even more but unfortunately capped in price.

I have posted the fundamentals on the above stocks so the price movement should trend upwards in the medium term.

My loser: TM and CMMT ( down 2 % )

Sunday, November 7, 2010

AUD/MYR soar to 3.135 CRB index up 314

Congrats to those who bought into commodity currency AUD/MYR at 2.6, 2.8, 3.0 range

Commodity CRB index ( of precious metals, industrial metals, oil, grains) has surge to 314, up from 270 since August while US Dollar index has slide from 82 to 76 in the same period. Go directly to website www.ino.com or click on Market Summary: US Index under Market Update on the right side column of this blog.

Wednesday, November 3, 2010

How to assess Plantation Co. EPS wrt CPO price movement

Cepat Wawasan Plant (nta RM1.69, Q/Q eps 1.6/ 2.7/ 2.5/ 1.3/ 4.1 sen )

Puzzled over the jump in Q eps, I looked into the company's website info. Info derived from the plantation operation webpage suggest 133, 044 mt fresh fruit bunches (FFB) harvested and milling operation webpage suggest 314,569 mt FFB processed..?

Which is which...? Either a grave error or they are processing/extracting for other smaller planters and deriving a profit.

Anyway, annual production FY 2009, FFB = 133,044 mt. Estimated extraction of CPO = 0.2 x FFB = 26,609 mt

CPO mt/ share = 26, 609/ 215,450,000 shares issued = 0.12 mt/1000 shares

For every RM100/mt increase in CPO, annual EPS = RM100 x 0.12/1000 = 0.012 or 1.2 sen accretive

Therefore up target price (PE 10) = 12 sen

HS Plant (nta RM2.14, Q/Q eps 2.9/ 5/ 4.6/ 4.5 sen )

Production FY 2009, FB = 672, 768 mt. Estimated CPO = 0.21 x FFB = 140,985 mt

CPO mt/ share = 140, 985 / 800 million = 0.17 mt/ 1000 shares

For every RM100/mt up, it adds 1.7 sen to annual EPS . TP up 17 sen

Puzzled over the jump in Q eps, I looked into the company's website info. Info derived from the plantation operation webpage suggest 133, 044 mt fresh fruit bunches (FFB) harvested and milling operation webpage suggest 314,569 mt FFB processed..?

Which is which...? Either a grave error or they are processing/extracting for other smaller planters and deriving a profit.

Anyway, annual production FY 2009, FFB = 133,044 mt. Estimated extraction of CPO = 0.2 x FFB = 26,609 mt

CPO mt/ share = 26, 609/ 215,450,000 shares issued = 0.12 mt/1000 shares

For every RM100/mt increase in CPO, annual EPS = RM100 x 0.12/1000 = 0.012 or 1.2 sen accretive

Therefore up target price (PE 10) = 12 sen

HS Plant (nta RM2.14, Q/Q eps 2.9/ 5/ 4.6/ 4.5 sen )

Production FY 2009, FB = 672, 768 mt. Estimated CPO = 0.21 x FFB = 140,985 mt

CPO mt/ share = 140, 985 / 800 million = 0.17 mt/ 1000 shares

For every RM100/mt up, it adds 1.7 sen to annual EPS . TP up 17 sen

Monday, October 25, 2010

HunzPty

Hunza Properties posted quarterly gain/ (profit plus capital revaluation) of approx. RM 34.69 m

Q eps = RM 34.69m/ 194m shares = 17.8 sen

Bear in mind that RM 22.7m is due to revaluation gain of Penang Paragon under FRIS 140 accounting, therefore actual properties sales profit is only RM 12m which works out to be 6.2 sen Q eps (ie. RM 12m/ 194m shares). This is a 13% drop from Q/Q eps of 7.1 sen

Declares dv 5.6 sen ex. 31st Dec . Maintain buy at RM1.60

Q eps = RM 34.69m/ 194m shares = 17.8 sen

Bear in mind that RM 22.7m is due to revaluation gain of Penang Paragon under FRIS 140 accounting, therefore actual properties sales profit is only RM 12m which works out to be 6.2 sen Q eps (ie. RM 12m/ 194m shares). This is a 13% drop from Q/Q eps of 7.1 sen

Declares dv 5.6 sen ex. 31st Dec . Maintain buy at RM1.60

Monday, October 18, 2010

CMMT Reits. Property Co. Steel Cos. on my radar

CMMT just posted their maiden earning of Q eps of 6 sen. Assuming quarterly earnings can be maintained and with annualised PER of 10, fair value Fv = 6 x 4 x 10 = RM2.40

Comparatively AXreit, UOAreit, Qcap, ARreit, STAreit have PER ranging from 11 to 13. So CMMT is a buy for me at RM1.09

Sunrise (nta RM 2.21, Q eps 7.8 sen ) Assume PE 10, Fv = 3.12

Suncity (nta RM5.21, Q eps 15 sen ) Fv = RM 6.00

DNP (nta RM 2.35, Q eps 6 sen ) Fv = RM 2.40

Hunza (nta RM 2.30, Q eps 7 sen ) Fv = RM 3.20

Lion Ind (nta RM 4.25, Q/Q eps 10/11/12/17 sen ). Trading at PE of 4

MaSteel (nta RM 2.12, Q/Q eps 7/5/3/4 sen ). Trading at PE of 5

Kinsteel (nta RM 0.89, Q/Q eps 2/4/2/1 sen ). Trading at PE of 11

Leader (nta RM 1.25, Q/Q eps 4/3/2/3 sen ). Trading at PE of 8

Comparatively AXreit, UOAreit, Qcap, ARreit, STAreit have PER ranging from 11 to 13. So CMMT is a buy for me at RM1.09

Sunrise (nta RM 2.21, Q eps 7.8 sen ) Assume PE 10, Fv = 3.12

Suncity (nta RM5.21, Q eps 15 sen ) Fv = RM 6.00

DNP (nta RM 2.35, Q eps 6 sen ) Fv = RM 2.40

Hunza (nta RM 2.30, Q eps 7 sen ) Fv = RM 3.20

Lion Ind (nta RM 4.25, Q/Q eps 10/11/12/17 sen ). Trading at PE of 4

MaSteel (nta RM 2.12, Q/Q eps 7/5/3/4 sen ). Trading at PE of 5

Kinsteel (nta RM 0.89, Q/Q eps 2/4/2/1 sen ). Trading at PE of 11

Leader (nta RM 1.25, Q/Q eps 4/3/2/3 sen ). Trading at PE of 8

Sunday, October 10, 2010

A Check on TM & Axiata Earnings

TM (nta RM 2.07, Q/Q eps 5.1sen, 4.8sen, 6.9sen, 3.5sen in August). Earning in August not that great, dropped by 50%... Trading at PE 20 is expensive..!

Let's see if new Uni-Fi subscriptions can improve near future earning.

Axiata (nta RM 2.23, Q/Q eps 6 sen, 7sen, 11sen, 7 sen in August). Quarterly earning declined by 35%... Trading at PE 15... Will buy on dips..

While USD has tumbled against most currencies, other currencies has strengthen more than MYR. Few months back AUD used to be 2.8 MYR, SGD was 2.3 MYR. Now they have move up to almost 3.1 and 2.4 respectively. What does this tells me...?

AUD and USD is close to parity... Could it be flight to commodity currencies, carry trade to higher yielding currencies.....?

Let's see if new Uni-Fi subscriptions can improve near future earning.

Axiata (nta RM 2.23, Q/Q eps 6 sen, 7sen, 11sen, 7 sen in August). Quarterly earning declined by 35%... Trading at PE 15... Will buy on dips..

While USD has tumbled against most currencies, other currencies has strengthen more than MYR. Few months back AUD used to be 2.8 MYR, SGD was 2.3 MYR. Now they have move up to almost 3.1 and 2.4 respectively. What does this tells me...?

AUD and USD is close to parity... Could it be flight to commodity currencies, carry trade to higher yielding currencies.....?

Wednesday, October 6, 2010

Earnings Drop: Top Glove

Top Glove just released their quarterly earning

Net profit approx. RM 43 million, a 30% decline compared to their previous RM 64 million

Therefore earning per share, Qeps = RM 43m/ 618m shares issued = RM 0.073 or 7.3 sen

My fair value Fv = 7.3 x 4 x 10 = RM 2.92. So at RM 5.70, it's expensive for my liking.

Speculating on Supermax similar decline of 30% net profit

Net profit = 70% x last quarter RM 45 million = RM 32 m

Q eps = RM 32m/ 339 m shares = RM 0.095 or 9.5 sen

My fair value Fv = 9.5 x 4 x 10 = RM 3.80

I'll be comfortable to buy around RM3.30 when it slides from the current RM 4.26

Net profit approx. RM 43 million, a 30% decline compared to their previous RM 64 million

Therefore earning per share, Qeps = RM 43m/ 618m shares issued = RM 0.073 or 7.3 sen

My fair value Fv = 7.3 x 4 x 10 = RM 2.92. So at RM 5.70, it's expensive for my liking.

Speculating on Supermax similar decline of 30% net profit

Net profit = 70% x last quarter RM 45 million = RM 32 m

Q eps = RM 32m/ 339 m shares = RM 0.095 or 9.5 sen

My fair value Fv = 9.5 x 4 x 10 = RM 3.80

I'll be comfortable to buy around RM3.30 when it slides from the current RM 4.26

Thursday, September 23, 2010

SP Setia. Glomac

SP Setia (nta RM2.07, Qeps 5.6, 3.8, 5.0, 8.6 sen latest) Fv = RM3.20

At RM4.50 its PE is approx 14

Glomac (RM1.94, Qeps 3.6, 4.2, 5.3 sen latest) Fv = RM2.00

AtRM1.50 PE is approx 8

At RM4.50 its PE is approx 14

Glomac (RM1.94, Qeps 3.6, 4.2, 5.3 sen latest) Fv = RM2.00

AtRM1.50 PE is approx 8

Thursday, August 26, 2010

QL Reso. PPB. MBB. CIMB

QL (nta RM1.35 Qeps 6.9sen ) Fv = 7 x 4 x assumed PER 10 = RM 2.80

At current price of RM4.50 it's PER = 16. Declares dividend Dps = 7 sen

PPB (nta RM11.93 Qeps 26.8) Fv = 27 x 4 x 10 = RM 10.80

A current price of RM17.00 it;s PER = 16. Declares Dps = 70 sen ex. 8/9

Better to invest in companies whose business is in soft commodities (plant-based produce like corns, sugarcane, flour, edible oil and livestock farming produce) rather than hard commodities (base/industrial metals) at the moment.

Maybank (nta RM 3.94 prev Qeps 14.6sen recent Qeps 12.9 sen) Fv = RM 5.20

At RM 8.20 , PER = 16. Declares Dps = 44 sen

CIMB ( nta RM 2.93 prev Qeps 23.7sen recent Qeps 12.6 sen) Fv = RM 5.00

At RM 7.70 , PER = 15. Declares Dps = 4.6 sen

At current price of RM4.50 it's PER = 16. Declares dividend Dps = 7 sen

PPB (nta RM11.93 Qeps 26.8) Fv = 27 x 4 x 10 = RM 10.80

A current price of RM17.00 it;s PER = 16. Declares Dps = 70 sen ex. 8/9

Better to invest in companies whose business is in soft commodities (plant-based produce like corns, sugarcane, flour, edible oil and livestock farming produce) rather than hard commodities (base/industrial metals) at the moment.

Maybank (nta RM 3.94 prev Qeps 14.6sen recent Qeps 12.9 sen) Fv = RM 5.20

At RM 8.20 , PER = 16. Declares Dps = 44 sen

CIMB ( nta RM 2.93 prev Qeps 23.7sen recent Qeps 12.6 sen) Fv = RM 5.00

At RM 7.70 , PER = 15. Declares Dps = 4.6 sen

Sunday, August 22, 2010

Capital Protected Unit Trust Funds

Beware of the terms & conditions when you do invest in capital protected trust fund.

You may not get your money back immediately after the maturity period. It does vary from institution to institution but just beware, it's not what it seems in terms of liquidity and projected gain.

Take for example, ING Capital Protected Baraka Fund . Maturing in early July 2010 after 3 years, it has not pay out the money to its investors. It has a hidden built-in clause (not disclosed verbally by its sales personnel at time of sales) that permits it to to take as long as 2 months after its maturity to return the money to its investors.

The fund has not performed as projected (min 6% to max 30%) but instead has yielded zero gain to its investors.

Lesson for all..?

No two trust funds are alike so choose carefully. Have the sales staff to explain in details the prospectus, if necessary, page by page. Look at the historic performance of the company trust funds bearing in mind that good fund managers are always head-hunted and pinched so there's no guarantee that previous performance of the funds can be extrapolated.

Learn to handle your own investments. Trade the market and start by investing in dividends paying stock counters. Learn from the many bloggers who share their ideas and opinions so unselfishly. Start small and invest consistently. And don't worry too much about price fluctuation when buying into good companies, eg. if you think TM at RM3.50 is expensive then what do you think will be its price in 5 years, 10 years, 15 years period when your kids grow up to buy into the stock market...?

happy invest....

You may not get your money back immediately after the maturity period. It does vary from institution to institution but just beware, it's not what it seems in terms of liquidity and projected gain.

Take for example, ING Capital Protected Baraka Fund . Maturing in early July 2010 after 3 years, it has not pay out the money to its investors. It has a hidden built-in clause (not disclosed verbally by its sales personnel at time of sales) that permits it to to take as long as 2 months after its maturity to return the money to its investors.

The fund has not performed as projected (min 6% to max 30%) but instead has yielded zero gain to its investors.

Lesson for all..?

No two trust funds are alike so choose carefully. Have the sales staff to explain in details the prospectus, if necessary, page by page. Look at the historic performance of the company trust funds bearing in mind that good fund managers are always head-hunted and pinched so there's no guarantee that previous performance of the funds can be extrapolated.

Learn to handle your own investments. Trade the market and start by investing in dividends paying stock counters. Learn from the many bloggers who share their ideas and opinions so unselfishly. Start small and invest consistently. And don't worry too much about price fluctuation when buying into good companies, eg. if you think TM at RM3.50 is expensive then what do you think will be its price in 5 years, 10 years, 15 years period when your kids grow up to buy into the stock market...?

happy invest....

Monday, August 16, 2010

GenM. Axiata. TM. Boustead

Sold some GenM at RM3.08

Still think GenM should be around RM3.30 (earning is similar to Jerneh's last quarter earning)

Collecting Axiata, TM, Boustead

Still cheapest blue chip on the KLSE

Still think fund manager will use GenM, Axiata, TM to stage rally. Crazy maybe.

Still think GenM should be around RM3.30 (earning is similar to Jerneh's last quarter earning)

Collecting Axiata, TM, Boustead

Still cheapest blue chip on the KLSE

Still think fund manager will use GenM, Axiata, TM to stage rally. Crazy maybe.

Saturday, July 24, 2010

Boustead. TM.

Boustead's dividend payout record: 5 sen on 26th June 2009, 5 sen on 13th Sept 2009, 7.5 sen on 11th Dec 2009, final 10 sen on16th Mar 2010. Recent payout 5 sen on 15th Jun.

I think we can expect another 5 sen come early Sept.

TM's dividend payout: 10 sen on 8th Sept 2009. Recent payout 13 sen on 18th May.

Expecting a minimum 10 sen end Sept.

I think we can expect another 5 sen come early Sept.

TM's dividend payout: 10 sen on 8th Sept 2009. Recent payout 13 sen on 18th May.

Expecting a minimum 10 sen end Sept.

Monday, July 5, 2010

Sime vs. IOI

Sime (Last four Q eps 16/11/7/ -5 sen). Quarterly earnings decline with the recent at a loss. Sold my holding much earlier when I saw the earning drop from 11 sen to 7. What's the fair value to buy in again..? Assuming becomes profitable in the next two quarters at Q eps 7 sen, then fair value Fv (with annualised PER 10) = 7 x 4 x 10 = RM2.80

Current price of Sime = RM7.49 ie. at 2.67 times over its fair value of PER 10

Check IOI (Q eps 8.2/8.0/7.7/8.6 sen recent) Fair value Fv = 8.6 x 4 x 10 = RM3.44

Current price of IOI = RM4.95

Ratio 495/ 344 = 1.44, so IOI is currently priced at 14.4 PER

Applying same ratio, Sime should be priced at 1.44 x RM2.80 = RM4.04

For now, IOI seems to have better value than Sime

Current price of Sime = RM7.49 ie. at 2.67 times over its fair value of PER 10

Check IOI (Q eps 8.2/8.0/7.7/8.6 sen recent) Fair value Fv = 8.6 x 4 x 10 = RM3.44

Current price of IOI = RM4.95

Ratio 495/ 344 = 1.44, so IOI is currently priced at 14.4 PER

Applying same ratio, Sime should be priced at 1.44 x RM2.80 = RM4.04

For now, IOI seems to have better value than Sime

Friday, July 2, 2010

June's Job Losses Up, May's Factory Orders Drop

The US economy lost 125,000 jobs in June, more than financial market and economist's forecast of 110,000 as thousands of temporary census jobs ended and private hiring grew less than expected.

With unemployment stubbornly high, household spending has turned sluggish in recent months, threatening to create a vicious cycle that stock market investors and some analysts worry could tip the economy back into recession.

The Federal Reserve is also in a bind. It has held benchmark overnight interest rates close to zero since December 2008 and has pumped more than $1 trillion into the economy.

Fed officials believe a sustainable recovery has taken hold, but are watching cautiously.

Orders to U.S. factories declined broadly in May after nine straight months of gains, raising new concerns that the recovery is stalling. The Commerce Department said Friday that orders for manufactured goods decreased 1.4 percent in May. It was the biggest drop since March 2009.

With unemployment stubbornly high, household spending has turned sluggish in recent months, threatening to create a vicious cycle that stock market investors and some analysts worry could tip the economy back into recession.

The Federal Reserve is also in a bind. It has held benchmark overnight interest rates close to zero since December 2008 and has pumped more than $1 trillion into the economy.

Fed officials believe a sustainable recovery has taken hold, but are watching cautiously.

Orders to U.S. factories declined broadly in May after nine straight months of gains, raising new concerns that the recovery is stalling. The Commerce Department said Friday that orders for manufactured goods decreased 1.4 percent in May. It was the biggest drop since March 2009.

Tuesday, June 29, 2010

G20 to cut deficits by 2013

G20 countries vow to slash their budget deficits by half by 2013 and stabilses the government debt/GDP ratio by 2016. That's the general consensus reached by leaders of the G20 forum in Canada recently.

This means less and lesser Gov't spending on infrastructure, reduced priming of the economy by quantitative easing (money supply or printing) and gradual withdrawal of subsidies, welfare, healthcare, grants.

But reduction on spending will impact growth and lower growth means lesser revenue for the Gov't. Slower growth will hamper employment , lower wages resulting in more labour union strikes and street riots. This is not positive for both the global market and Gov't.

Gov't may increase rates for tax, duties and tariff which negate regional competitiveness and thus making exports expensive.

Simply bad news...

This means less and lesser Gov't spending on infrastructure, reduced priming of the economy by quantitative easing (money supply or printing) and gradual withdrawal of subsidies, welfare, healthcare, grants.

But reduction on spending will impact growth and lower growth means lesser revenue for the Gov't. Slower growth will hamper employment , lower wages resulting in more labour union strikes and street riots. This is not positive for both the global market and Gov't.

Gov't may increase rates for tax, duties and tariff which negate regional competitiveness and thus making exports expensive.

Simply bad news...

Sunday, June 27, 2010

Glovemakers Earnings Review

Top Gloves (Q/Q/latest Qeps 22/23/ latest 21 sen, nta RM 3.37) Earnings Q/Q flat over 3 quarters. Fair value Fv with annualised PER 10 = 21 x 4 x 10 = RM8.40

Supermax (Q/Q/ latest Qeps 15/16/ 19 sen, nta RM2.33) Earnings up but is it sustainable..?. Fv = 7.60 Revised Fv =7.60/1.25 = RM6.10 adjusted after 25% bonus issue.

Kossan (Q/Q/ latest Qeps 9/15/ 19sen, nta RM2.33) Earnings up. Fv =RM 7.60

Latexx (Q/Q/latest Qeps 7/9/ 10.5 sen, nta RM0.99) Earnings up. Fv = RM 4.20

Adventa (Q/Q/latest Qeps 3.7/6.4/ 4.6 sen, nta RM 1.36) Earnings decline. Fv = RM 1.90

Current prices: Top Gloves RM13.00 Supermax RM5.90 Kossan RM7.60 Latexx RM3.60 Adventa RM3.20

Supermax (Q/Q/ latest Qeps 15/16/ 19 sen, nta RM2.33) Earnings up but is it sustainable..?. Fv = 7.60 Revised Fv =7.60/1.25 = RM6.10 adjusted after 25% bonus issue.

Kossan (Q/Q/ latest Qeps 9/15/ 19sen, nta RM2.33) Earnings up. Fv =RM 7.60

Latexx (Q/Q/latest Qeps 7/9/ 10.5 sen, nta RM0.99) Earnings up. Fv = RM 4.20

Adventa (Q/Q/latest Qeps 3.7/6.4/ 4.6 sen, nta RM 1.36) Earnings decline. Fv = RM 1.90

Friday, June 11, 2010

Strategy : Dividend stocks

Save yourself some stress, buy into dividend counters.

My strategy for next 3 months = focus on dividend stocks.

Looking to buy on dips: TM, Boustead, HapSeng Cons., HS Plant, HunzPty, TDM, Efficien

A few others caught my attention: Manulife, WTHorse, Ascotec, FPI

My current portfolio: Axiata, Boustead, Digi, Esso, Efficien, GenM, HapSeng, HSPlant, Hubline, Hunza, IGB, IJM, LionInd, QL Reso, TDM, THPlant, TM

Sold all of Supermax, looking to switch to GenM, TM and Axiata (three of cheapest priced blue chips, not necessary in value). I'm buying to hold for 10 years (trading on price volatility), seriously.

I'll be watching price action of construction, materials, property stocks.

My strategy for next 3 months = focus on dividend stocks.

Looking to buy on dips: TM, Boustead, HapSeng Cons., HS Plant, HunzPty, TDM, Efficien

A few others caught my attention: Manulife, WTHorse, Ascotec, FPI

My current portfolio: Axiata, Boustead, Digi, Esso, Efficien, GenM, HapSeng, HSPlant, Hubline, Hunza, IGB, IJM, LionInd, QL Reso, TDM, THPlant, TM

Sold all of Supermax, looking to switch to GenM, TM and Axiata (three of cheapest priced blue chips, not necessary in value). I'm buying to hold for 10 years (trading on price volatility), seriously.

I'll be watching price action of construction, materials, property stocks.

Friday, June 4, 2010

Markets tumble on weak jobs data

US stocks felled sharply on Friday after May payrolls indicates private hiring was lower than expected, raising fears of the strength of the economic recovery.

Labor department reported 431,000 jobs was added to the US economy but of that total, 411,000 was hired for US Census (jobs which are short term and temporal): falling short of the 513,000 expected by Wall Street.

This shows that there is no much economic ability to generate ongoing job growth and that raises question of sustainability of the recovery, " said Joseph Battipaglia, market strategist at Stifel Nicolaus in Yardley Pennsylvania.

Labor department reported 431,000 jobs was added to the US economy but of that total, 411,000 was hired for US Census (jobs which are short term and temporal): falling short of the 513,000 expected by Wall Street.

This shows that there is no much economic ability to generate ongoing job growth and that raises question of sustainability of the recovery, " said Joseph Battipaglia, market strategist at Stifel Nicolaus in Yardley Pennsylvania

Monday, May 31, 2010

Quick News: Gold at USD1,700/ oz

Greece Central Bank is selling one ounce equivalents as high as USD 1,700 (40% over spot price) and prices on the black markets higher as people unload their paper assets stocks and bonds on fear of the nation's government defaulting on their own debts.

Punchline:- hold on to your gold, buy a little when it dips, sell as needed in times of paper currency collapse.

Punchline:- hold on to your gold, buy a little when it dips, sell as needed in times of paper currency collapse.

Sunday, May 30, 2010

Earnings: Axiata.TM.Sunway.HapSeng.HSPlant.Bstead.MSing

Axiata ( Qeps 11 sen cf. previous Qeps 7 sen, nta 219 ) Fv = 11 x 4Q x PE10 = RM 4.40

TM ( Qeps 6.9 sen cf. previous Qeps 4.8 sen, nta 213) Fv = 6.9 x 4 x 10 = RM 2.76

Sunway (Qeps 6.9 sen cf. previous Qeps 4.2 sen, nta 132) Fv = 6.9 x 4 x 10 = RM 2.76

HapSeng Cons (Qeps 7 sen cf. previous Qeps 1.4 sen, nta 422 ) Fv = 7 x 4 x 10 = RM 2.80

HSPlant ( Q/Q eps 4.5/5.0 sen, nta 215) Fv = RM 1.80

Boustead ( Q/Q eps 9.7/16.2sen, nta 427 ) Fv = 9.7 x 4 x 10 = RM 3.88

Dv 5 sen t.e. ex. 15th June

MahSing (Q/Q eps 4.0/3.9, nta 126) Fv = 4 x 40 = 160

TM ( Qeps 6.9 sen cf. previous Qeps 4.8 sen, nta 213) Fv = 6.9 x 4 x 10 = RM 2.76

Sunway (Qeps 6.9 sen cf. previous Qeps 4.2 sen, nta 132) Fv = 6.9 x 4 x 10 = RM 2.76

HapSeng Cons (Qeps 7 sen cf. previous Qeps 1.4 sen, nta 422 ) Fv = 7 x 4 x 10 = RM 2.80

HSPlant ( Q/Q eps 4.5/5.0 sen, nta 215) Fv = RM 1.80

Boustead ( Q/Q eps 9.7/16.2sen, nta 427 ) Fv = 9.7 x 4 x 10 = RM 3.88

Dv 5 sen t.e. ex. 15th June

MahSing (Q/Q eps 4.0/3.9, nta 126) Fv = 4 x 40 = 160

Friday, May 21, 2010

Euro rescue: Eyes on Germany as lawmakers vote

BERLIN (AP) -- With the future of the euro in the balance, German lawmakers were expected Friday to approve the massive rescue deal to save the common currency and contain the debt crisis -- a signal that the finance minister said was needed to reassure jittery markets.

Both houses of parliament were scheduled to vote on the euro750 billion (nearly $1 trillion) package drawn up two weeks ago and Chancellor Angela Merkel's center-right government currently holds a majority in each.

Germany, Europe's biggest economy, is to contribute between euro123 billion and euro147.6 billion in loan guarantees. It comes hard of the heels of a separate package to rescue Greece -- which was already unpopular, given that Germans dislike the idea of paying for others' financial missteps.

"We have to put into effect what we have agreed, because markets will only trust when it is actually in effect," Finance Minister Wolfgang Schaeuble told lawmakers. "The reality is that the markets look more at Germany than at Cyprus or Malta ... so it is right, in order to win markets' confidence, that we decide so quickly."

Merkel had called for lawmakers' approval on Wednesday, declaring that "if the euro fails, then Europe fails." "We are not doing this out of generosity toward others; we are doing this in our own best national interest," Schaeuble said. "And this national interest means remaining integrated into a Europe growing further together."

Nearly two-thirds of German exports go to other eurozone countries, and "if we didn't have the common currency, we would have much less economic potential, less prosperity and less social security," he added.

Both houses of parliament were scheduled to vote on the euro750 billion (nearly $1 trillion) package drawn up two weeks ago and Chancellor Angela Merkel's center-right government currently holds a majority in each.

Germany, Europe's biggest economy, is to contribute between euro123 billion and euro147.6 billion in loan guarantees. It comes hard of the heels of a separate package to rescue Greece -- which was already unpopular, given that Germans dislike the idea of paying for others' financial missteps.

"We have to put into effect what we have agreed, because markets will only trust when it is actually in effect," Finance Minister Wolfgang Schaeuble told lawmakers. "The reality is that the markets look more at Germany than at Cyprus or Malta ... so it is right, in order to win markets' confidence, that we decide so quickly."

Merkel had called for lawmakers' approval on Wednesday, declaring that "if the euro fails, then Europe fails." "We are not doing this out of generosity toward others; we are doing this in our own best national interest," Schaeuble said. "And this national interest means remaining integrated into a Europe growing further together."

Nearly two-thirds of German exports go to other eurozone countries, and "if we didn't have the common currency, we would have much less economic potential, less prosperity and less social security," he added.

Tuesday, May 18, 2010

AUD falls sharply

AUD slip to 2.79 on concern about Europe's debt crisis and possible slowdown in China's demand for Australia's resources.

Friday, May 14, 2010

Forget Eurozone... this country could be the next to suffer a debt crisis

Now that the Greek debt crisis has been "fixed" by a gigantic pile of more debt, many are wondering which European nation will be next to experience a massive debt crisis.

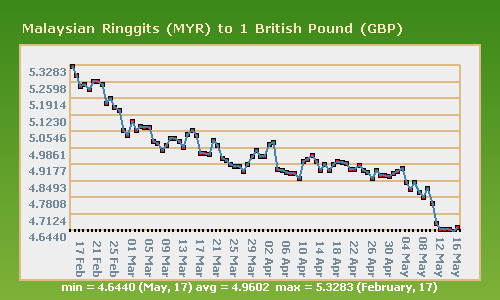

GBP at 4.65 MYR

GBP at 4.65 MYR

Increasingly, all eyes are turning to the U.K. and their public debt that is spiralling out of control. The U.K. government's deficit is projected to be approximately 13 percent of GDP in 2010, which is even worse than Greece's 12.5 percent figure. Right now the public debt of the U.K. is...http://theeconomiccollapseblog.com/archives/will-the-u-k-be-the-next-european-nation-to-experience-a-massive-debt-crisis

GBP at 4.65 MYR

GBP at 4.65 MYRIncreasingly, all eyes are turning to the U.K. and their public debt that is spiralling out of control. The U.K. government's deficit is projected to be approximately 13 percent of GDP in 2010, which is even worse than Greece's 12.5 percent figure. Right now the public debt of the U.K. is...http://theeconomiccollapseblog.com/archives/will-the-u-k-be-the-next-european-nation-to-experience-a-massive-debt-crisis

Friday, May 7, 2010

TM maintains dividend payout

Telekom Malaysia Bhd (TM) (4863)says it wants to continue dishing out around RM700 million in dividends, or over 90 per cent of its net profit, to shareholders annually.

TM and the government will each fork out RM1 billion this year to further develop the country's high speed broadband service, branded "UniFi". They had agreed to invest equally in the first few years, TM chief executive officer Datuk Zamzamzairani Mohd Isa said. TM and the government together spent RM1.9 billion last year, he told reporters after its annual general meeting in Kuala Lumpur yesterday.

"We will maintain annual dividend payout of RM700 million, or over 90 per cent of our patami (profit after tax and minority interests), whichever is higher," he said. TM has announced a total dividend of RM706.5 million, or 19.75 sen net per share, for its financial year ended December 31 2009.

TM and the government will each fork out RM1 billion this year to further develop the country's high speed broadband service, branded "UniFi". They had agreed to invest equally in the first few years, TM chief executive officer Datuk Zamzamzairani Mohd Isa said. TM and the government together spent RM1.9 billion last year, he told reporters after its annual general meeting in Kuala Lumpur yesterday.

"We will maintain annual dividend payout of RM700 million, or over 90 per cent of our patami (profit after tax and minority interests), whichever is higher," he said. TM has announced a total dividend of RM706.5 million, or 19.75 sen net per share, for its financial year ended December 31 2009.

Monday, May 3, 2010

In News: Latexx. SSteel. HunzPty.DiGi

LATEXX PARTNERS BHD more than doubled its net profit to RM20.72 million for the first quarter ended March 31, 2010 (1QFY10) from RM9.14 million a year earlier on the back of capacity expansion, aggressive marketing strategy and overall cost savings.Revenue surged 79.4% to RM126.17 million from RM70.32 million, while earnings per share rose to 10.52 sen from 4.7 sen. It declared a tax exempt interim dividend of 2.5 sen per share.

SOUTHERN STEEL BHD posted a net profit of RM34.48 million in its first quarter ended March 31, 2010, versus a net loss of RM65.48 million a year earlier on the back of a higher revenue in line with the economic recovery.Revenue surged 59.74% to RM628.74 million from RM393.6 million, while pre-tax profit totaled RM37.1 million versus a loss of RM78.5 million a year earlier. Basic earnings per share stood at 8.2 sen, versus a loss per share of 15.6 sen previously.

Penang-based Hunza Properties Bhd’s net profit surged 95.26% to RM11.29mil for the quarter ended March 31, 2010 compared with the previous corresponding period on higher property sales and contributions from the Gurney Paragon project.

The company said in an announcement to Bursa Malaysia yesterday that revenue for the quarter jumped 214% to RM58.52mil.

DIGI.COM BHD net profit for the first quarter ended March 31, 2010 rose to RM278.26 million from RM275.44 million a year ago, on the back of a 6% increase in revenue to RM1.3 billion. The company had on Tuesday, May 4 also declared a first interim dividend payout of 35 sen per ordinary share of 10 sen each, payable on June 18, 2010. Earnings per share rose to 35.80 sen from 35.40 sen a year earlier, while net assets per share was RM1.77.

SOUTHERN STEEL BHD posted a net profit of RM34.48 million in its first quarter ended March 31, 2010, versus a net loss of RM65.48 million a year earlier on the back of a higher revenue in line with the economic recovery.Revenue surged 59.74% to RM628.74 million from RM393.6 million, while pre-tax profit totaled RM37.1 million versus a loss of RM78.5 million a year earlier. Basic earnings per share stood at 8.2 sen, versus a loss per share of 15.6 sen previously.

Penang-based Hunza Properties Bhd’s net profit surged 95.26% to RM11.29mil for the quarter ended March 31, 2010 compared with the previous corresponding period on higher property sales and contributions from the Gurney Paragon project.

The company said in an announcement to Bursa Malaysia yesterday that revenue for the quarter jumped 214% to RM58.52mil.

DIGI.COM BHD net profit for the first quarter ended March 31, 2010 rose to RM278.26 million from RM275.44 million a year ago, on the back of a 6% increase in revenue to RM1.3 billion. The company had on Tuesday, May 4 also declared a first interim dividend payout of 35 sen per ordinary share of 10 sen each, payable on June 18, 2010. Earnings per share rose to 35.80 sen from 35.40 sen a year earlier, while net assets per share was RM1.77.

Repayment of Amortized Loan

Here's an amortization calculator formula for deriving the amount of monthly repayment taken against a loan/ mortgage.

A = P { i + i / [(( 1 + i ) pw. n) - 1]}

Where: A = periodic payment amount, P = principal amount, i = periodic decimal interest rate ( not percentage), pw. = to the power, n = total number of periodic payments.

eg. P = RM400000, i = 3.6% per annum ( 0.036 pa or 0.003 pm), n = 20 years ( 240 mths).

A= 400,000 {0.003 + 0.003 /[ ((1 + 0.003) pw. 240) - 1]} = 400,000 {0.003 + 0.003/[2.05222- 1]} = 2340.44

So annual repayment = RM2,340.44 x 240 months for RM400,000 loan at 3.6% mortgage rate

A = P { i + i / [(( 1 + i ) pw. n) - 1]}

Where: A = periodic payment amount, P = principal amount, i = periodic decimal interest rate ( not percentage), pw. = to the power, n = total number of periodic payments.

eg. P = RM400000, i = 3.6% per annum ( 0.036 pa or 0.003 pm), n = 20 years ( 240 mths).

A= 400,000 {0.003 + 0.003 /[ ((1 + 0.003) pw. 240) - 1]} = 400,000 {0.003 + 0.003/[2.05222- 1]} = 2340.44

So annual repayment = RM2,340.44 x 240 months for RM400,000 loan at 3.6% mortgage rate

Tuesday, April 20, 2010

ASN funds online top up service by CIMB

Permodalan Nasional Bhd and CIMB Bank today unveiled CIMB Clicks Amanah Saham Nasional Bhd (ASNB) Funds Top Up Facility at the 11th Minggu Saham Amanah Malaysia (MSAM) in Kuching.

The online facility allows all registered ASNB investors, who have a CIMB Clicks account to make additional investments in five fixed-price unit trust funds managed by ASNB.

The five funds are Amanah Saham Bumiputera (ASB), Amanah Saham Malaysia (ASM), Amanah Saham Didik (ASD), Amanah Saham Wawasan 2020 (ASW2020) and Amanah Saham 1Malaysia (AS 1Malaysia).

Read more: CIMB offers online ASN funds top up service http://www.btimes.com.my/Current_News/BTIMES/articles/20100420153853/Article/index_html#ixzz0lXGza0pH

The online facility allows all registered ASNB investors, who have a CIMB Clicks account to make additional investments in five fixed-price unit trust funds managed by ASNB.

The five funds are Amanah Saham Bumiputera (ASB), Amanah Saham Malaysia (ASM), Amanah Saham Didik (ASD), Amanah Saham Wawasan 2020 (ASW2020) and Amanah Saham 1Malaysia (AS 1Malaysia).

Read more: CIMB offers online ASN funds top up service http://www.btimes.com.my/Current_News/BTIMES/articles/20100420153853/Article/index_html#ixzz0lXGza0pH

Wednesday, April 14, 2010

News: Telekom. Supermax. MaSteel

The Employees Provident Fund, Malaysia’s largest pension fund, bought 5.5 million shares in Telekom Malaysia Bhd, between April 5 and 6, raising the fund’s stake in Telekom, the nation’s biggest fixed line operator, to 11 per cent, according to a stock exchange filing. -- Bloomberg

Supermax Corp Bhd is optimistic of a bullish financial performance this year as its expects earnings per share (EPS) for the first quarter of 2010 to exceed its earnings guidance for the year. Executive chairman cum group managing director Datuk Seri Stanley Thai said the company was revising its EPS target from a minimum of 50 sen per share to a minimum of 62 sen per share for the financial year ending Dec 31, 2010. He said the revised profit guidance for the current year took into account latex price fluctuations, foreign exchange and the possibility of a hike in natural gas and electricity tariffs.

Malaysia Steel Works (KL) Bhd (Masteel) expects its overseas revenue contribution to grow by 65 per cent in 2012 from the 30 per cent at present following the completion of its downstream expansion.

Supermax Corp Bhd is optimistic of a bullish financial performance this year as its expects earnings per share (EPS) for the first quarter of 2010 to exceed its earnings guidance for the year. Executive chairman cum group managing director Datuk Seri Stanley Thai said the company was revising its EPS target from a minimum of 50 sen per share to a minimum of 62 sen per share for the financial year ending Dec 31, 2010. He said the revised profit guidance for the current year took into account latex price fluctuations, foreign exchange and the possibility of a hike in natural gas and electricity tariffs.

Malaysia Steel Works (KL) Bhd (Masteel) expects its overseas revenue contribution to grow by 65 per cent in 2012 from the 30 per cent at present following the completion of its downstream expansion.

Friday, April 9, 2010

Telekom declares 13 sen dvd

TM declares 13 sen (less 25% tax, 9.7 sen net) dividend ex. 18th May

This year alone, it has declared a total of 10 sen tax exempted + today 9.7 sen net = 19.7 sen

If you have bought in at RM 3.00, that is a dividend yield of 19.7/ 300 = 6.56 %

with capital appreciation of RM3.50 (today's price)/ RM 3.00 = 16.7 %

making a total of approx 23 % in less than a year...

That's RM 23,000 for every RM 100,000 invested, in less than a year...

This year alone, it has declared a total of 10 sen tax exempted + today 9.7 sen net = 19.7 sen

If you have bought in at RM 3.00, that is a dividend yield of 19.7/ 300 = 6.56 %

with capital appreciation of RM3.50 (today's price)/ RM 3.00 = 16.7 %

making a total of approx 23 % in less than a year...

That's RM 23,000 for every RM 100,000 invested, in less than a year...

Thursday, April 8, 2010

My Favorite Glovemaker

Supermax (Q eps 16.4 sen, nta RM 2.08). Simple Fv = 16.4 x 4 x 10 = RM 6.56: Today's price at RM7.10, approx PER 10.8 <*** top value ***>

Latexx (Q eps 8.8 sen, nta RM 0.87). Simple Fv = RM 3.52: Today price at RM 4.00, approx PER 11.3

Kossan (Q eps 15 sen, nta RM 2.23). Simple Fv = RM 6.00: Today's price at RM 8.00, approx PER 13.3

Top Glove (Q eps 23.5 sen, nta RM 3.02). Simple Fv = RM 9.40 : Today's price at RM13.60, approx PER 14.5

Sunday, April 4, 2010

Still Buying

Market may take a dip, come Monday and Tuesday. I'll be buying.

A firm buy for me, the following counters:

TM, Axiata, MayBk, CIMB, Supermax, GenM, TDM, HunzPty, Lion Ind

That's because I'm purchasing on "averaging up" .

I have these in my existing holding at much lower prices.

CIMB was a recent acquistion at recent high: like it for its regional reach, deals, book making, Thai IPO (for dividend repayment..?), bonus issue 1:1. Hold for 3 years, double up...?

Still like MayBk, because everyone I meet hates MayBk.

Good Q eps, PER trailing that of CIMB and Public Bk.

A wise person once told me that banks are the life lines of the country's economy.

Sectors I like in 2010: banks, utility, healthcare, property & construction, building materials

A firm buy for me, the following counters:

TM, Axiata, MayBk, CIMB, Supermax, GenM, TDM, HunzPty, Lion Ind

That's because I'm purchasing on "averaging up" .

I have these in my existing holding at much lower prices.

CIMB was a recent acquistion at recent high: like it for its regional reach, deals, book making, Thai IPO (for dividend repayment..?), bonus issue 1:1. Hold for 3 years, double up...?

Still like MayBk, because everyone I meet hates MayBk.

Good Q eps, PER trailing that of CIMB and Public Bk.

A wise person once told me that banks are the life lines of the country's economy.

Sectors I like in 2010: banks, utility, healthcare, property & construction, building materials

Wednesday, March 31, 2010

In the News: Supermax, Maybank, MRCB, POS, MPHB

Supermax Corp, a Malaysian rubber glove maker, said it raised its internal after-tax profit target to RM168 million for 2010 from RM136 million, to reflect higher demand for its products, following US healthcare reforms.

Malayan Banking Bhd's (Maybank) dividend re-investment plan, expected to be effective in 2Q 2010, is a better option compared with the rights issue in strengthening its share capital base and capital position, said its chief executive officer, Datuk Seri Abdul Wahid Omar. He said Maybank’s policy was to pay between 40 and -60 per cent of its profit after tax and minority interest as dividend.

Chief executive officer Mohamed Razeek Hussain Mericar said Malaysian Resources Corp (MRCB) wants to participate in a plan by the government and the Employees Provident Fund to form a venture to promote the development of 3,000 acres of government land in Sungai Buloh, outside Kuala Lumpur.

The comment comes after Prime Minister Datuk Seri Najib Razak said yesterday that the government and the Employees Provident Fund, the biggest shareholder of Malaysian Resources, will form a joint venture to promote the development of the land.

The government's investment arm, Khazanah Nasional Bhd, hopes to conclude the divestment of a 32.2 per cent stake in Pos Malaysia Bhd within this year. It was reported that the 32 per cent Pos Malaysia stake is worth about RM390 million.

Shares of Multi-Purpose Holdings Bhd, a Malaysian betting and financial services group, are worth as much as RM3.24 each to reflect its plan to roll out property projects this year, CIMB Investment Bank Bhd said. -- Bloomberg

Malayan Banking Bhd's (Maybank) dividend re-investment plan, expected to be effective in 2Q 2010, is a better option compared with the rights issue in strengthening its share capital base and capital position, said its chief executive officer, Datuk Seri Abdul Wahid Omar. He said Maybank’s policy was to pay between 40 and -60 per cent of its profit after tax and minority interest as dividend.

Chief executive officer Mohamed Razeek Hussain Mericar said Malaysian Resources Corp (MRCB) wants to participate in a plan by the government and the Employees Provident Fund to form a venture to promote the development of 3,000 acres of government land in Sungai Buloh, outside Kuala Lumpur.

The comment comes after Prime Minister Datuk Seri Najib Razak said yesterday that the government and the Employees Provident Fund, the biggest shareholder of Malaysian Resources, will form a joint venture to promote the development of the land.

The government's investment arm, Khazanah Nasional Bhd, hopes to conclude the divestment of a 32.2 per cent stake in Pos Malaysia Bhd within this year. It was reported that the 32 per cent Pos Malaysia stake is worth about RM390 million.

Shares of Multi-Purpose Holdings Bhd, a Malaysian betting and financial services group, are worth as much as RM3.24 each to reflect its plan to roll out property projects this year, CIMB Investment Bank Bhd said. -- Bloomberg

The Web is Killing Polar Bears

The 'cloud' of data that is becoming the heart of the Internet is creating an all-too-real cloud of pollution as Facebook, Apple and others build data centers powered by coal, Greenpeace said in a new report to be released on Tuesday.

A Facebook facility being built in Oregon will rely on a utility whose main fuel is coal, while Apple is building a data warehouse in a North Carolina region that relies mostly on coal, the environmental organization said in the study.

"The last thing we need is for more cloud infrastructure to be built in places where it increases demand for dirty coal-fired power,'' said Greenpeace, which argues that Web companies should be more careful about where they build and should lobby more in Washington for clean energy.

The growing mass of business data, home movies and pictures has ballooned beyond the capabilities of many corporate data centers and personal computers, spurring the creation of massive server farms that make up a "cloud,'' an emerging phenomenon known as cloud computing.

Data center energy use already is huge, Greenpeace said.

If considered as a country, global telecommunications and data centers behind cloud computing would have ranked fifth in the world for energy use in 2007, behind the United States, China, Russia and Japan, it concluded.

If considered as a country, global telecommunications and data centers behind cloud computing would have ranked fifth in the world for energy use in 2007, behind the United States, China, Russia and Japan, it concluded.

Tuesday, March 30, 2010

Axiata: XL stake sale to pay for dividend

Axiata Group Bhd, Malaysia’s second-best performing index stock this year, may use proceeds from selling a 20 per cent stake in Indonesia’s PT XL Axiata to pay a dividend and repay debt, Chief Executive Officer Datuk Jamaludin Ibrahim said in an interview in Kuala Lumpur today.

It may also sell between RM1 billion and RM1.5 billion in Islamic bonds to refinance debt, he said. - Bloomberg

I'm buying in more of Axiata (for near future maiden dvd, regional telco play, analyst re-rating) and TM (potential future growth earnings, dvd of 11 sen soon..?). Both are fairly valued and not really expensive considering DiGi and Maxis are priced at PER 17 and PER 20 respectively. Buy only for the really long term if you're cash loaded.

Why I like mobile telco..?

1)- not almost anyone has a house or can buy a house, but almost everyone has a mobile cellphone in their pocket or can afford to buy one. 2)- cellphones are becoming indispensible for social communication or as a communication tool: you wouldn't think of leaving home without it.

Why I like TM...?

1)- it's pure monopoly in the ground/fixed line business. 2)- it's irreplaceable in business communication as most businesses still carry a ground line for voice/fax transmission. 3)- I think it's still cheaper to chat using ground line than mobile line (apart from VOIP, Skype etc) so many aunties/ grandmas are still keeping their TM phone at home. 4)- Future growth earnings albeit slowly as an alternative to pay-TV Astro etc as HSBB becomes reality.

It may also sell between RM1 billion and RM1.5 billion in Islamic bonds to refinance debt, he said. - Bloomberg

I'm buying in more of Axiata (for near future maiden dvd, regional telco play, analyst re-rating) and TM (potential future growth earnings, dvd of 11 sen soon..?). Both are fairly valued and not really expensive considering DiGi and Maxis are priced at PER 17 and PER 20 respectively. Buy only for the really long term if you're cash loaded.

Why I like mobile telco..?

1)- not almost anyone has a house or can buy a house, but almost everyone has a mobile cellphone in their pocket or can afford to buy one. 2)- cellphones are becoming indispensible for social communication or as a communication tool: you wouldn't think of leaving home without it.

Why I like TM...?

1)- it's pure monopoly in the ground/fixed line business. 2)- it's irreplaceable in business communication as most businesses still carry a ground line for voice/fax transmission. 3)- I think it's still cheaper to chat using ground line than mobile line (apart from VOIP, Skype etc) so many aunties/ grandmas are still keeping their TM phone at home. 4)- Future growth earnings albeit slowly as an alternative to pay-TV Astro etc as HSBB becomes reality.

Thursday, March 25, 2010

Steel-Making Co. Q eps. Fair value

Some of the steel-making companies quarterly earnings.

Lion Ind (Q eps 11.7 sen, nta RM 3.97). Fv = 11 x 4 x 10 = RM 4.68

At RM 1.75, it's very attractively priced at 38 % of fair value or annualised PER 3.8

Lion Div (Q eps 5.7 sen, nta RM 1.78) . Fv = RM 2.28, today's price RM 0.44 PER 1.9

Southern Steel (Q eps 14.2 sen, nta RM 1.80). Fv = RM 5.68, today's price RM 2.46 PER 4.5

CSC Steel (Q eps 9.9 sen, nta RM 2.09). Fv = RM 3.96, today's price at RM 1.76 PER 4.4

MaSteel (Qeps 5.4 sen, nta RM 2.14), Fv = RM 2.16, today's price RM 1.09 PER 5

Kinsteel (Q eps 4.4 sen, nta RM 0.85). Fv = RM 1.76, today's price RM 1.02 PER 5.8

Ann Joo Reso (Q eps 4.5 sen, nta RM 1.80). Fv = RM 1.80, today's price RM 2.70 PER 15

So guess which counter offers the best value..?

Lion Ind (Q eps 11.7 sen, nta RM 3.97). Fv = 11 x 4 x 10 = RM 4.68

At RM 1.75, it's very attractively priced at 38 % of fair value or annualised PER 3.8

Lion Div (Q eps 5.7 sen, nta RM 1.78) . Fv = RM 2.28, today's price RM 0.44 PER 1.9

Southern Steel (Q eps 14.2 sen, nta RM 1.80). Fv = RM 5.68, today's price RM 2.46 PER 4.5

CSC Steel (Q eps 9.9 sen, nta RM 2.09). Fv = RM 3.96, today's price at RM 1.76 PER 4.4

MaSteel (Qeps 5.4 sen, nta RM 2.14), Fv = RM 2.16, today's price RM 1.09 PER 5

Kinsteel (Q eps 4.4 sen, nta RM 0.85). Fv = RM 1.76, today's price RM 1.02 PER 5.8

Ann Joo Reso (Q eps 4.5 sen, nta RM 1.80). Fv = RM 1.80, today's price RM 2.70 PER 15

So guess which counter offers the best value..?

Monday, March 22, 2010

UEM Land RI @ 80 sen. ASM unitholders get 6.3 sen

UEM Land Holdings Bhd, a Malaysian developer, priced its proposed rights issue shares at 80 sen each, which is a 44.1 per cent discount to the stock’s recent average price, the company said in a statement to the Kuala Lumpur stock exchange.UEM Land said it hopes to raise gross proceeds of RM971.3 million from the one-for-two rights issue. CIMB Group Holdings Bhd and Malayan Investment Bank Bhd were appointed joint underwriters, it said. -- Bloomberg

Amanah Saham Nasional Bhd (ASNB) today announced an income distribution of 6.30 sen per unit for Amanah Saham Malaysia (ASM) for the financial year ended March 31, 2010.

The income distribution will be reinvested in additional ASM units to be automatically credited into the unitholders'' accounts on April 1, 2010.

ASM is a fixed priced equity-income fund aimed at providing unitholders with a long-term investment opportunity that generates regular and competitive returns through a diversified portfolio of investments. -- Bernama

Amanah Saham Nasional Bhd (ASNB) today announced an income distribution of 6.30 sen per unit for Amanah Saham Malaysia (ASM) for the financial year ended March 31, 2010.

The income distribution will be reinvested in additional ASM units to be automatically credited into the unitholders'' accounts on April 1, 2010.

ASM is a fixed priced equity-income fund aimed at providing unitholders with a long-term investment opportunity that generates regular and competitive returns through a diversified portfolio of investments. -- Bernama

Saturday, March 20, 2010

Plantation Co. Quarterly EPS 2

HS Plant (latest Q eps 5 sen, nta RM 2.10). Fv = 5 x 4 x 10 = RM2.00

At RM2.40 it's fairly priced (@ PER 12), given its historic 5 sen dividend tax exempted to be declared on both June and Oct. I'm expecting a 5 sen dvd tax-exempted this June.

Assume 10 sen tax-exempted, dvd yield = 10 sen/240 = 4.17%

TH Plant (latest Q eps 4.6 sen, nta RM0.93). Fv = 4.6 x 4 x 10 = RM1.84

At RM1.55 it's fairly attractive, considering it may pay 8.5 sen dvd taxable in this May

IJM Plant (latest Q eps 5.2 sen, nta RM1.48). Fv = 5.2 x 4 x 10 = RM2.08

At RM2.50 it's fairly priced (@ PER 12). I think it may not pay the usual dvd of 8 sen in July as it expands its land bank in Indonesia; typical of a good growth stock capex.

Kim Loong (latest Q eps 4.8 sen, nta RM1.39). Fv = 4.8 x 4 x 10 =RM1.92

At RM2.15 it's fairly priced over PER of 11. Usual dvd payout 3 sen in Jul, 4 sen in Nov.

TSH Plant (latest Q eps 5.4, nta RM 1.78). Fv = 5.4 x 4 x 10 = RM2.16

At RM2.06 it's fairly attractive. Usual dvd payout of 5 sen in Jun

Unico Plant (latest Q eps 1.7 sen, nta RM0.88). Fv = 1.7 x 4 x 10 = RM0.68

At RM0.82, it's priced at PER of 12. Usual dvd payout of 2 sen in March and 2 sen in Oct

If you have bought in at RM0.80, dvd yield annualised 4 sen/80 sen = 5 %

Important to note: Investing in Plantation Co. is for the very long term investor.

Catalyst: Adverse weather resulting in dwindling CPO causing price surge. Tracks Soya bean oil as agri alternative and Crude Oil as bio fuel alternatives.

Demographic changes causing scarcity of land banks for agri, manufacturing, infra-structure and housing development. Land banks of plantation companies appreciate in value and surge when converted to development land.

Happy investing...! May Jesus Christ bless you richly in spirit, mind, heart, physique, family relationship, schools, business and in your finance..

J = X

At RM2.40 it's fairly priced (@ PER 12), given its historic 5 sen dividend tax exempted to be declared on both June and Oct. I'm expecting a 5 sen dvd tax-exempted this June.

Assume 10 sen tax-exempted, dvd yield = 10 sen/240 = 4.17%

TH Plant (latest Q eps 4.6 sen, nta RM0.93). Fv = 4.6 x 4 x 10 = RM1.84

At RM1.55 it's fairly attractive, considering it may pay 8.5 sen dvd taxable in this May

IJM Plant (latest Q eps 5.2 sen, nta RM1.48). Fv = 5.2 x 4 x 10 = RM2.08

At RM2.50 it's fairly priced (@ PER 12). I think it may not pay the usual dvd of 8 sen in July as it expands its land bank in Indonesia; typical of a good growth stock capex.

Kim Loong (latest Q eps 4.8 sen, nta RM1.39). Fv = 4.8 x 4 x 10 =RM1.92

At RM2.15 it's fairly priced over PER of 11. Usual dvd payout 3 sen in Jul, 4 sen in Nov.

TSH Plant (latest Q eps 5.4, nta RM 1.78). Fv = 5.4 x 4 x 10 = RM2.16

At RM2.06 it's fairly attractive. Usual dvd payout of 5 sen in Jun

Unico Plant (latest Q eps 1.7 sen, nta RM0.88). Fv = 1.7 x 4 x 10 = RM0.68

At RM0.82, it's priced at PER of 12. Usual dvd payout of 2 sen in March and 2 sen in Oct

If you have bought in at RM0.80, dvd yield annualised 4 sen/80 sen = 5 %

Important to note: Investing in Plantation Co. is for the very long term investor.

Catalyst: Adverse weather resulting in dwindling CPO causing price surge. Tracks Soya bean oil as agri alternative and Crude Oil as bio fuel alternatives.

Demographic changes causing scarcity of land banks for agri, manufacturing, infra-structure and housing development. Land banks of plantation companies appreciate in value and surge when converted to development land.

Happy investing...! May Jesus Christ bless you richly in spirit, mind, heart, physique, family relationship, schools, business and in your finance..

J = X

Plantation Co. Quarterly EPS

Here's a simple analysis to determine if the stock shares you intend to buy is undervalued or overpriced. First find out its Quaterly earning per share (Q eps). Then multiply by 4 to estimate its annualised/yearly earnings. Then multiply by PE ratio 10. (PE Ratio simply means the price I paid for its share today, the company should in 10 years time match it with all its accumulated earnings, theorectically).

So simple Fair Value or Price = Q eps x 4 x 10.

Boustead (latest Q eps 16.2 sen, nta RM4.20). Fair Value Fv = 16 x 4 x 10 = RM6.40

At RM3.40 ( ex. 16/3, 6 sen t.e. + 4 sen taxable), it's very attractively priced at abt 55% of its fair value. The only issue is whether the Q eps is sustainable in the following quaters.

TDM (latest Q eps 9.7 sen, nta RM2.88 ). Fv = 9.7 x 4 x 10 = RM3.88

At RM1.70, it's attractively priced at 46% of its Fv. Still holding on to mine as I expect it to declare 14 sen dividend (approx. 8 %) in June.

Will post HS Plant, TH Plant, IJM Plant, Unico, Kim Loong, TSH later or 2moro...

So simple Fair Value or Price = Q eps x 4 x 10.

Boustead (latest Q eps 16.2 sen, nta RM4.20). Fair Value Fv = 16 x 4 x 10 = RM6.40